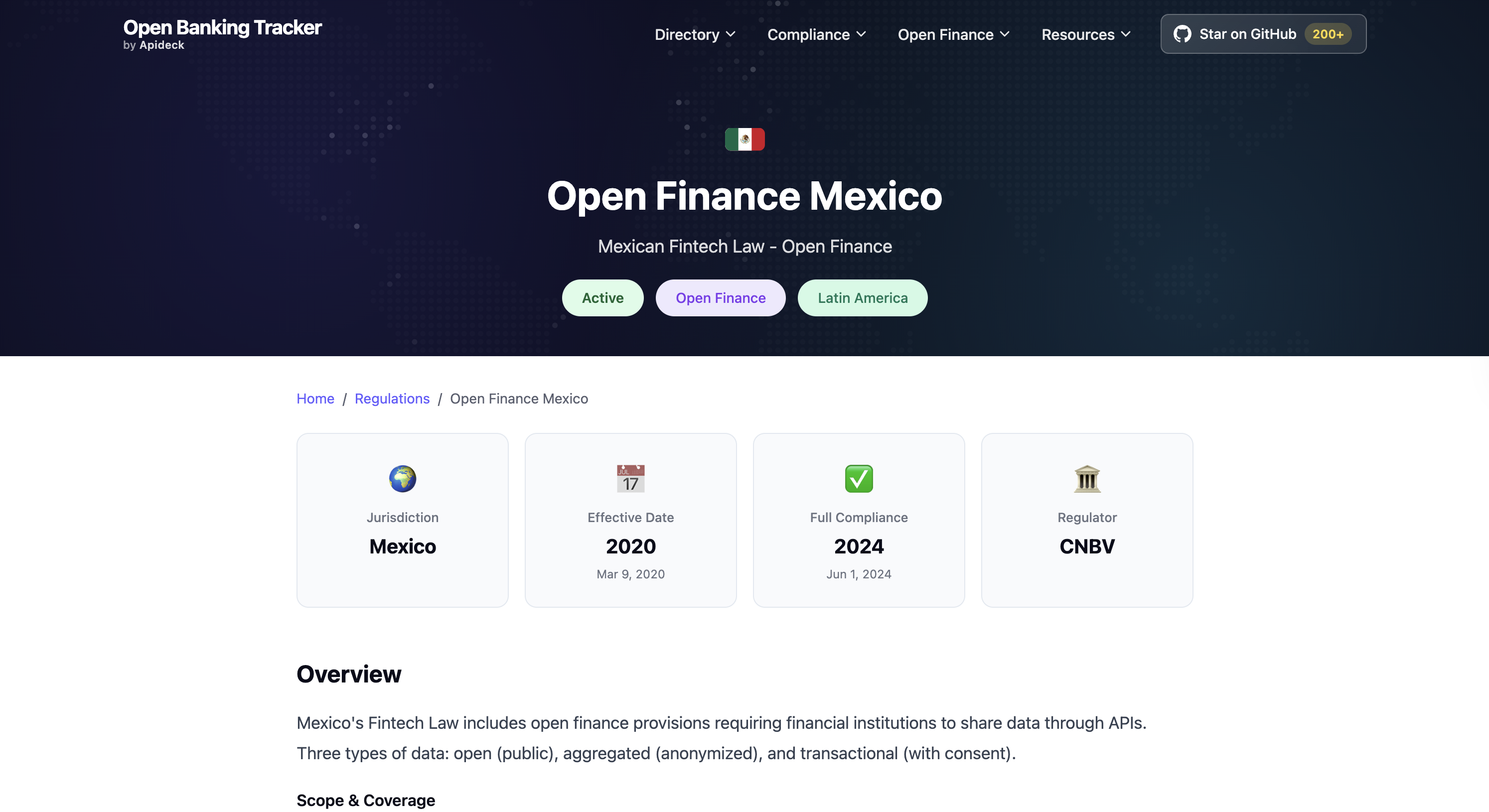

Mexico passed its Fintech Law in March 2018. At the time, it was the most ambitious open banking legislation in Latin America. The law required banks, fintechs, money transmitters, and credit bureaus to build standardized APIs for sharing open financial data, aggregated data, and transactional data. Eight years later, the secondary regulations needed to actually enforce most of those requirements still have not been issued.

The only secondary regulation published so far covers open data for ATMs. That is it. No binding rules for transactional data sharing. No mandatory consent frameworks. No accreditation standards for third-party providers. The Fintech Law wrote the check. The regulators have not cashed it.

This is not a minor bureaucratic delay. It has real consequences for a country where, according to the ENIF 2024 survey from INEGI and the CNBV, roughly 20% of adults still lack access to any formal financial product. Mexico has 795 active local fintechs as of the end of 2025, per a report from the trade association FinTech Mexico. Another 316 foreign entities operate in the country, bringing the total above 1,100 according to the Finnovista Fintech Radar Mexico 2026. Many of these companies rely on fintech APIs for payments, lending, and accounting integrations, but without standardized open banking rails, each integration is bespoke. The ecosystem is ready. The rules are not.

What the Fintech Law actually says

The 2018 law established a framework for two types of licensed fintech entities: electronic payment fund institutions (IFPEs, essentially digital wallets) and crowdfunding platforms. It also created a regulatory sandbox for novel business models, though as of 2025, no entities have been authorized through the sandbox according to multiple industry analyses. That is seven years of a sandbox sitting empty.

On open banking specifically, the law mandated that financial institutions share three tiers of data through APIs. Open data (product catalogs, ATM locations, fees) was the first tier and the only one with published secondary regulation. Aggregated data (anonymized, statistical) and transactional data (account-level, consent-driven) still await their rules.

The CNBV, Mexico's banking and securities commission, and Banxico, the central bank, are the lead regulators. The CNBV did commission a pilot project with DAI and the Open Bank Project (TESOBE) to test transactional and consent API guidelines in a simulated environment. The pilot produced technical specifications. But those specifications have not been adopted as binding regulation.

Meanwhile, the World Bank published a technical note with a roadmap for open finance implementation in Mexico covering 2023 to 2025. That window has closed. The roadmap's milestones remain largely unmet.

The fintech ecosystem grew anyway

The regulatory gap has not stopped Mexico's fintech market from expanding. It has, however, shaped what that expansion looks like.

Nu Mexico (Nubank's subsidiary) had approximately 12 million clients by 2025 and announced its ten millionth loan in January of that year. Spin, the financial arm of Oxxo's convenience store network, onboarded more than 12 million clients by September 2024. Klar raised $190 million and Plata raised $410 million in 2025 to consolidate their neobanking positions. These are real numbers from named companies operating at scale.

The Finnovista Fintech Radar Mexico 2026 found that 70% of Mexican fintechs have been operating for more than five years. Revenue across the ecosystem grew 31% in the 2023-2024 period, according to the Finnovista Fintech Radar Mexico 2025. The mortality rate is low, around 5%. And 77% of fintechs in the 2026 report have integrated AI into their business models, up from 68% in 2025.

Payments and remittances remain the biggest segment. In 2024, 45% of fintechs in this category processed more than $30 million in digital transactions each. That figure is expected to reach 76% by 2027.

The growth is happening through bilateral integrations, proprietary data pipelines, and direct bank partnerships. What it is not happening through is a standardized, regulated open banking infrastructure. Every fintech that wants access to bank data today has to negotiate it one institution at a time. That is expensive, slow, and inherently exclusionary toward smaller players. The embedded finance model has grown fast in Mexico precisely because it sidesteps this bottleneck.

Remittances: the $62 billion use case nobody can unlock

Mexico received $61.8 billion in remittances in 2025, according to Banxico data reported by BBVA Research. That figure was actually a 4.6% decline from the record $64.7 billion in 2024, ending an 11-year streak of consecutive growth. The decline was the largest since 2009.

Even with the drop, remittances still represent roughly 3.4% of Mexico's GDP. Electronic transfers account for 99.1% of the total. But of the money received electronically, 49.6% was still collected in cash. That split tells you something important: the pipes are digital, but the last mile is not.

Open banking could change that equation. If recipients could connect their remittance inflows directly to savings products, credit scoring, or insurance through consent-driven data sharing, the financial inclusion impact would be immediate. The business use cases for open banking are well documented in other markets. Mexico just cannot access them yet. A mother in Michoacan who receives $400 a month from her son in Chicago should be able to use that income history to qualify for a loan or build a savings plan without visiting a bank branch.

The average remittance fee in the US-Mexico corridor is slightly below 5% for a $200 transfer, according to World Bank data from Q1 2025. The UN's target is 3%. Fintech competition (Bitso claims it processed over $6.5 billion in remittances in 2024) is pushing fees down, but open banking rails could accelerate that further by reducing the cost of identity verification and account linking. The money movement infrastructure needed to make this work at scale already exists in other markets.

The Trump administration's immigration policies, including a 1% remittance tax in the One Big Beautiful Bill Act (signed July 4, 2025, effective January 1, 2026), add new uncertainty to these flows. The tax applies to cash, money orders, and cashier's checks but exempts transfers from US bank accounts or funded by US-issued debit and credit cards. That exemption limits the direct impact, but the signal it sends to remittance-dependent households is real. BBVA Research identified three major risks for 2026: a potential US economic slowdown, aggressive immigration enforcement, and peso appreciation. In this environment, making every dollar of remittance income more useful through better financial products is more than an abstract policy goal.

Brazil and Colombia pulled ahead

The comparison with Brazil is instructive. Brazil launched its open finance ecosystem in phases starting in February 2021 and reached operational maturity by 2024, with comprehensive governance structures under BCB Resolution No. 400. The framework extends well beyond banking data into insurance, investments, and pensions.

Colombia published a comprehensive mandatory open finance draft decree in June 2025, moving from a voluntary framework to a regulated one. The Superintendencia Financiera de Colombia and the Financial Regulation Unit are leading the implementation. Chile is also further along in defining its framework.

Mexico, which passed its open banking law three years before Brazil's regulations and five years before Colombia's decree, is now behind both in actual implementation. The Open Finance Map tracks 80+ regulatory frameworks globally, and Mexico's stands out as one of the oldest with the least operational output. According to the Ozone API 2025 assessment of Latin American open finance, open finance in Mexico is "back to the discussion" but the regulatory framework remains "under construction."

The Finnovista Radar Mexico 2026 noted a decline in the number of local open finance players, citing the lack of clear regulatory progress. Companies are pivoting their business models rather than waiting for rules that may not come soon.

What the CNBV is actually focused on

The CNBV has not been idle. It has been busy with other priorities. In June 2025, it decreed temporary managerial intervention on three financial institutions (CIBanco, Intercam Banco, and Vector Casa de Bolsa) after the US Treasury's FinCEN identified them as primary money laundering concerns. CIBanco's banking license was revoked in October 2025. The CNBV also introduced new fraud prevention regulations requiring financial institutions to implement fraud prevention plans and establish individual transaction limits.

In November 2025, Banxico and the CNBV presented a proposal to overhaul payment network regulation with an emphasis on interoperability and a cap on interchange fees. These reforms touch on bank API integration at the infrastructure level, but they do not address the data-sharing layer that open banking requires.

These are not trivial matters. AML enforcement and payment system reform are important. But they illustrate a pattern: open banking keeps getting deprioritized in favor of more urgent supervisory issues. The secondary regulations are always next, never now.

Nubank's Mexican subsidiary secured CNBV approval in April 2025 to begin the process of becoming a full-service bank. That approval took years of regulatory engagement. If the full banking license process requires that level of sustained effort for a single institution, the prospect of building a multi-party open finance infrastructure without dedicated regulatory bandwidth is hard to take seriously. Banks in other countries are already moving toward accounting and ERP integration as a competitive differentiator. Mexican banks cannot do the same without the API standards to build on.

What would actually move things forward

The usual prescription is "issue the secondary regulations." That is true but insufficient. Mexico needs at least three things to make open banking real.

A binding timeline for transactional data API standards, with consequences for non-compliance. The Fintech Law already provides the legal basis. The CNBV has the authority. What is missing is the political will to set a deadline and enforce it.

A working governance body that includes banks, fintechs, and consumer representatives. Brazil's model, where a governance structure coordinates technical standards and dispute resolution across hundreds of participants, provides a template. Mexico does not need to copy it exactly, but the principle of shared governance (not just shared aspiration) is essential.

And a practical approach to the consent and identity layer. Mexico has real data protection law (the Federal Law on Protection of Personal Data Held by Private Parties), but no operational consent management framework specific to financial data sharing. The concept of open accounting, where businesses share financial data with lenders and platforms through APIs, is already gaining traction in other markets. Mexico's regulatory vacuum means none of this is standardized. Without that, banks will continue to cite privacy concerns as a reason not to open their APIs, even when the Fintech Law requires them to.

The 80% of Mexican adults who now hold at least one financial product, per the ENIF 2024, did not get there because of open banking. They got there because fintechs like Nubank, Spin, Klar, and Stori built products around the regulatory vacuum. That is a credit to those companies. But it means the people who are hardest to reach, the remaining 20%, are being left to market forces that have limited incentive to serve them.

Open banking was supposed to lower the barriers. Eight years in, the barriers are still there. The Fintech Law is good legislation. It just needs someone to finish the job.

For a full overview of banks and financial institutions in Mexico with open banking APIs, visit the Open Banking Tracker Mexico page. To compare Mexico's progress against other markets, see the full list of countries tracked globally.