Wise reported a take rate of 58 basis points on cross-border volume in fiscal 2025, down from 67 bps a year earlier. The typical bank FX markup on a small international transfer sits around 300 basis points. Banks charge roughly five times what Wise does on the same flow and still lose the customer.

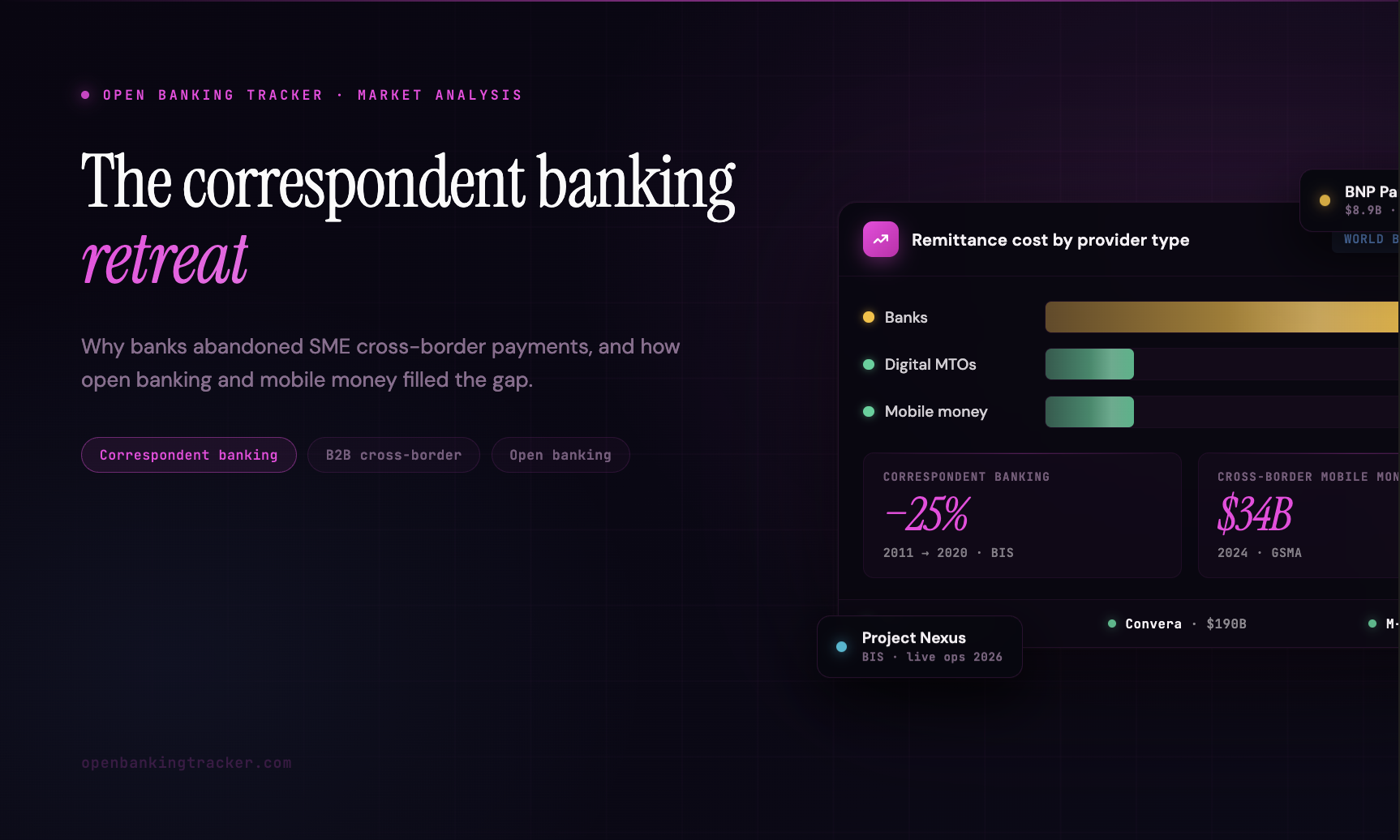

The World Bank's Remittance Prices Worldwide report for Q1 2025 tells the same story from a different angle. Banks charge an average of 14.55% to send a small international remittance. Digital-only money transfer operators average 3.55%. Banks are over four times more expensive than the fintechs they compete with, and they have responded by exiting the segment rather than competing on price.

That gap is the visible end of a longer story: the global retreat of correspondent banking from SME and consumer payments, and the rise of fintechs that filled the space.

What correspondent banking is, and why the retreat matters

A correspondent banking relationship is the account one bank holds with another in a different country to clear payments in foreign currencies. Most international wire transfers still route through this network, often passing through two or three intermediary banks before reaching the recipient. When a bank closes a correspondent account, every flow that depended on it has to find another path or stop. That has been happening at scale for over a decade.

The Bank for International Settlements reports that the number of active correspondent banking relationships globally declined about 25% between 2011 and 2020. Latin America and Oceania saw the steepest drops. Cross-border payment volume kept growing while the number of banks willing to handle the payments shrank. SMEs and remittance senders absorbed the brunt of the contraction.

There are six structural reasons banks left.

Compliance cost per cross-border transaction

KYC, AML, sanctions screening, and correspondent due diligence cost roughly the same on a $500 remittance as on a $5 million corporate wire. The economics only work above a certain ticket size. After the 2012 HSBC AML settlement and the 2014 BNP Paribas sanctions settlement, the cost of getting compliance wrong rose into the billions, with BNP alone paying $8.9 billion. Banks responded by raising the floor on what they were willing to process. Anything below that floor got dropped or pushed to a self-serve portal nobody used.

De-risking: banks pulled out of entire corridors

The decline in correspondent relationships did not happen evenly. A 2020 BIS Quarterly Review found that some jurisdictions lost a quarter to a third of their relationships while others lost almost none. Banks pulled out of corridors where compliance cost exceeded the revenue produced. Caribbean economies and several Pacific island states lost direct access entirely. The Financial Stability Board has been writing reports about the problem for ten years. The trend continued anyway.

SME economics: why small business cross-border payments don't fit

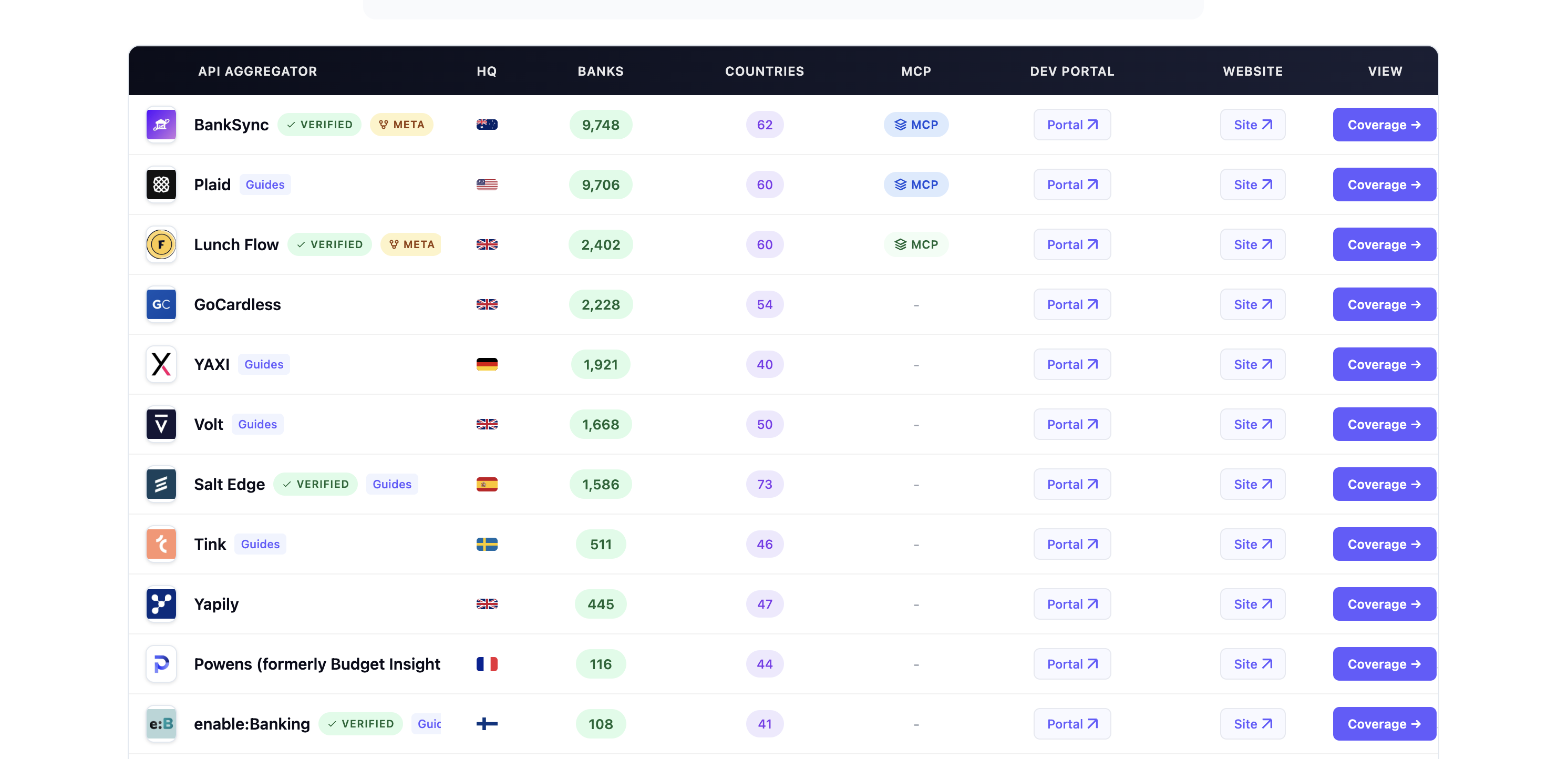

A mid-market SME doing $5 million in cross-border volume per year is a hard customer for a bank to serve. They need multi-currency accounts and hedging, plus someone to call when a payment gets stuck. They do not produce enough margin to justify a relationship manager, and they generate more support tickets than a corporate client doing $500 million. Banks staffed for corporates above a revenue threshold and pointed everyone below at a portal built in 2008. SMEs either tolerated it or moved to specialists. The embedded FX and cross-border directory on OBT lists the active players in this category.

Tech debt: SWIFT MT messages and batch settlement

Most banks still process cross-border payments on SWIFT MT messages and batch settlement systems they have not replaced in 20 years. Adding a modern cross-border product means either a multi-year core transformation or a sidecar that competes internally with the corporate FX desk. Both options have bad internal politics. JPMorgan built Onyx, now rebranded as Kinexys, anyway. Most banks chose not to invest at all.

Basel III and the regulatory capital problem

Cross-border exposures eat capital under Basel III. Holding nostro balances in 40 currencies to settle small tickets is a poor return on equity compared to mortgage lending or wealth management. A CFO at a Tier 1 bank looking at where to allocate scarce capital does not pick SME remittance. They pick the business with higher ROE and lower regulatory drag.

Distribution mismatch: phones, not branches

The customers banks abandoned are not the customers who walk into branches. Migrant workers sending remittances use phones. SMEs increasingly start with a fintech checking account before they ever talk to a bank. The acquisition channel moved from physical to digital, and most banks did not follow because their distribution was built around branch networks they were already trying to shrink. By the time the digital channel mattered, Wise and Revolut had already taken the segment.

What the Wise IPO made obvious

The Wise prospectus showed you could price cross-border FX at a fraction of bank rates and still run double-digit operating margins on a multi-billion pound volume base. The spread banks had been charging on small tickets came from market power, sustained by lack of competition. Once a credible alternative existed, the spread collapsed in the segments that mattered.

What banks kept is the part of the market they wanted: large corporates, financial institutions, and wholesale FX flows. Those still move through correspondent networks dominated by Citi and JPMorgan. The B2B cross-border payments market for SMEs and the consumer remittance market are gone, and they are not coming back.

Convera: even non-banks split B2B cross-border off

The bank retreat from B2B cross-border was not the only structural shift. In August 2021, Western Union sold its Business Solutions division for $910 million to a private equity consortium. The unit was renamed Convera and spun out as a standalone company, with the final close completing in 2023.

The logic mirrored the bank retreat, applied inside a non-bank. Western Union's core consumer remittance business ran on cash agent networks and small-ticket flows. The B2B unit served over 30,000 business and institutional customers across 140 currencies, with different operating models and customer needs. Combining them inside one company meant neither got the focus or investment it needed.

Convera now reports over $190 billion in annual turnover, with 2,100 employees across more than 30 offices. The point is not just that it competes with banks. Some banks that decided not to build their own cross-border products now route their customers' international payments through Convera on a white-label basis. The B2B cross-border layer banks gave up on is being supplied back to them by specialists.

How open banking changed the math

The retreat of correspondent banking happened in parallel with the rise of open banking. The two trends are causally linked.

Open banking gave cross-border fintechs two capabilities they did not have before. Payment Initiation Services (PIS) let a Wise or a Revolut pull funds directly from a sender's bank account, bypassing card rails and the fees that come with them. Account Information Services (AIS) made KYC and account verification close to instant, replacing manual onboarding flows that took days. Together they cut the cost of acquiring a cross-border customer by an order of magnitude.

The bigger structural shift came at the settlement layer. Wise and Revolut stopped using correspondent banking for retail flows altogether. They hold local balances in each major currency, funded through domestic instant payment systems on the inbound side. Outbound disbursement runs through the same rails. The cross-border element becomes a balance reconciliation problem on the back end rather than a real-time international wire.

That model only works in markets that built an open banking layer on top of a real-time domestic rail. The UK is the clearest example, pairing PSD2 with Faster Payments. Brazil shows the same pattern with open finance and Pix. In jurisdictions without either layer, cross-border remittance is still bank-dominated and expensive. Most of Sub-Saharan Africa falls into that group. OBT's open banking regulator directory shows which jurisdictions have a credible framework today.

For SMEs, the practical consequence is that the cross-border problem and the bank problem decoupled. A small business can keep its bank account for everything else and route international payments through Wise Business, Airwallex, or any provider plugged into the local open banking stack. Before PIS and AIS, switching costs were higher and bank cross-border services had a captive audience. Open banking removed the captivity.

Wallets: the rail open banking did not build

Open banking solved the funding-side problem in markets that have it. In markets that do not, mobile money wallets did the same thing through a different mechanism.

The GSMA 2025 industry report puts global mobile money transaction value at $1.68 trillion in 2024, with 2.1 billion registered accounts. Africa alone handled 65% of that volume. Cross-border remittances via mobile money reached $34 billion in 2024 at an average fee of 3.54%, lower than any other channel the World Bank tracks.

The model is straightforward. A sender in Kenya tops up their M-PESA wallet from a local agent. A remittance app like Wave debits the M-PESA balance through a partner API and credits a wallet on the receiving side. In Côte d'Ivoire that might be MTN MoMo. In Bangladesh it might be bKash. Local agents handle cash-out at the receive end. The cross-border element happens entirely outside the correspondent banking network.

Aggregators sit between wallets and bank rails to make this work at scale. Thunes connects more than 130 mobile money networks to bank accounts and cards. Nium does the same with a stronger SME focus. These companies do not appear in correspondent banking statistics because they do not need correspondent relationships. They have direct integrations with local payment providers in each market.

For SMEs, multi-currency fintech accounts at Wise Business or Airwallex play the same role mobile money plays for consumers. A single place to hold balances in 20-plus currencies, with all the cross-border conversion absorbed into the provider's own books. The customer never touches a correspondent banking relationship.

Banks did not build this layer. The combination of mobile money wallets and multi-currency fintech accounts routes around the bank cross-border network entirely in markets where it works, and aggregators connect the two.

Where this goes next

Two BIS projects are pushing on the remaining bank-controlled flows from opposite directions.

Project Agorá targets the wholesale side. The pilot tests whether tokenised commercial bank deposits and tokenised central bank money can compress correspondent banking from a multi-day, multi-intermediary process into atomic settlement in seconds. It includes 41 private financial institutions across seven jurisdictions. If it works, the banks running the pilot keep the wholesale FX and trade finance business they already dominate, but on a faster rail.

Project Nexus targets the retail side. The BIS Innovation Hub Singapore Centre is connecting the instant payment systems of five Asian economies into a single multilateral scheme, with Nexus Global Payments incorporated in Singapore in April 2025 to run the live operations. India's UPI alone gives Nexus a potential user base of over a billion. If Nexus scales beyond Asia, the fintechs already plugged into domestic rails get a global rail by default, and correspondent banking shrinks further on the SME and consumer side.

The banks running Project Agorá are presumably trying to avoid being on the wrong side of correspondent banking decline a second time.

FAQ

What is correspondent banking?

Correspondent banking is the arrangement where one bank holds an account with another bank in a different country to clear cross-border payments in foreign currencies. Most international wire transfers still route through this network. A single payment may pass through two or three intermediary banks, each charging a fee and adding settlement time. See the OBT glossary for related terms.

Why are bank cross-border fees so much higher than fintech fees?

Banks face fixed compliance and capital costs that do not scale down to small tickets. The World Bank's Q1 2025 report found banks average 14.55% on remittances, while digital-only money transfer operators average 3.55%. Fintechs built infrastructure specifically for small cross-border flows and avoid the correspondent banking network for most routes.

What is bank de-risking?

Bank de-risking is the practice of closing correspondent banking relationships, customer accounts, or whole corridors that compliance teams classify as high-risk relative to the revenue they produce. It accelerated after the 2012 HSBC and 2014 BNP Paribas settlements. The Financial Stability Board has tracked the effects on financial inclusion in developing economies for over a decade.

What role does open banking play in cross-border payments?

Open banking gives cross-border fintechs two capabilities banks could not easily match. Payment Initiation Services let a provider pull funds directly from a sender's bank account, avoiding card fees. Account Information Services make KYC and account verification close to instant. Combined with direct integration into domestic instant payment systems like Pix or Faster Payments, this lets a fintech run a cross-border product without correspondent banking on the funding side.

Who replaced banks in the SME cross-border market?

Wise Business and Airwallex took the bulk of the SME volume. Revolut Business and Payoneer cover adjacent segments like freelancers and marketplaces. For embedded FX infrastructure, Currencycloud and Convera lead at the API layer. The Open Banking Tracker FX directory lists the active providers by category.

Is correspondent banking going to disappear?

Not for wholesale flows. The largest banks still need correspondent networks for trade finance, FX, and securities settlement. Project Agorá is testing whether tokenised deposits and central bank money can compress correspondent banking from a multi-day, multi-intermediary process to atomic settlement in seconds. If that works, the wholesale side may consolidate around fewer, faster correspondent relationships rather than disappear.

What is Convera, and how is it different from Western Union?

Convera is the spun-off business-to-business cross-border payments arm of Western Union. Western Union sold its Business Solutions division to a private equity consortium in 2021 for $910 million. The unit was renamed Convera and now operates as an independent company, while Western Union kept its consumer remittance business. Convera reports over $190 billion in annual turnover and white-labels cross-border payment services to banks and other financial institutions.

How do mobile money wallets fit into cross-border payments?

Mobile money wallets like M-PESA and MTN MoMo give people in emerging markets a digital balance they can fund and disburse without a bank account. For cross-border, remittance fintechs debit the balance through partner APIs and credit a wallet on the receive side. The cross-border movement happens outside the correspondent banking network. GSMA reports cross-border mobile money remittances reached $34 billion in 2024 at an average fee of 3.54%, lower than any other channel.

For an active directory of licensed cross-border and FX payment providers by jurisdiction, see the Open Banking Tracker.