The category always outgrows its name.

We started with PSD2 APIs and a directory of banks. Over 8 years and millions of visitors later, the questions coming in look nothing like they did in 2017. People are still asking about payment APIs and bank connectivity, but increasingly also about accounting software connectors, e-invoicing mandates, and what "Open Finance" regulation actually looks like across 30+ jurisdictions.

Last month at Finovate Europe, we launched the Open Finance Map to reflect where things have moved.

80+ regulations. One interactive map.

The Open Finance Map is a filterable, interactive view of every open banking, open finance, and e-invoicing regulation we track globally. As of today, that's 80+ frameworks across six categories: Open Banking (34), E-Invoicing (31), Open Finance (16), Payment Services (5), Digital Identity (1), and Operational Resilience (1). You can filter by region, by status (Active, Upcoming, Proposed), and by type.

Each regulation links to a dedicated detail page with structured data: jurisdiction, regulatory type, current status, scope of coverage (AIS, PIS, CBPII, VRP, and more), effective dates, and plain-language descriptions.

70 of those regulations are active today. 18 are upcoming.

The active frameworks span everything from PSD2 and UK Open Banking to Open Finance Brasil, India's Account Aggregator framework, Singapore's SGFinDex, Saudi Arabia's Open Banking, and Australia's Consumer Data Right. The upcoming section is arguably the most strategically valuable part: PSD3 (provisionally agreed in November 2025, with compliance expected 2027-2028) and FIDA in the EU, the US CFPB's Section 1033 (phased rollout through 2030 on paper, though currently frozen by litigation and under reconsideration), Canada's Consumer-Driven Banking framework, and emerging initiatives across Colombia, Chile, South Africa, Kenya, the Philippines, and more.

The e-invoicing layer is new and, I think, underappreciated. Most of Europe will have mandatory e-invoicing within 5 years. Most of the founders I talk to aren't thinking about it yet. The map covers 50+ countries including Peppol network providers and EU eInvoicing mandates, because the regulatory surface area for financial data is expanding well beyond traditional account access. No other interactive regulatory map combines open banking and e-invoicing in one place.

Not just a map. A gateway to the full dataset.

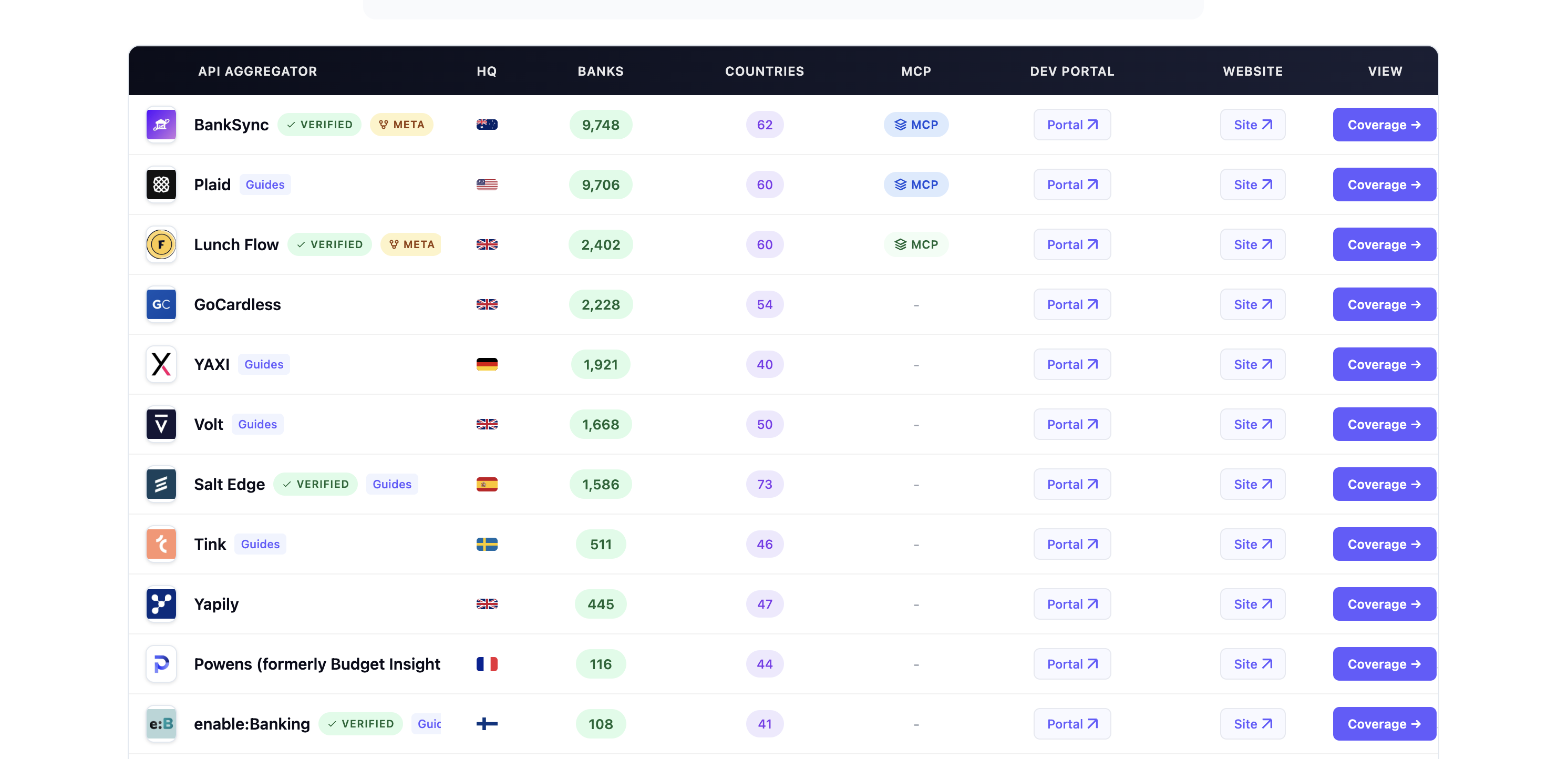

What makes this different from a static regulatory overview is what sits behind it. The Open Finance Map is backed by the Open Banking Tracker's full dataset: 54,776+ banks and financial institutions, 435+ third-party providers, 64+ API aggregators, and over 60 data points per institution.

You can drill from a regulation into the country page, then into individual institutions, their API availability, sandbox status, registered TPPs, and aggregator coverage. That depth of operational data behind an interactive regulatory map doesn't exist anywhere else.

The tracker started in 2017 as a PSD2 compliance tool. It now covers the full open finance ecosystem, from country-level regulatory intelligence to institution-level API data. The underlying data is open source on GitHub with nearly 200 stars and active community contributions.

A few observations from 8 years in this space

Payments are working in the UK. 33 million open banking payment transactions in November 2025 alone. 16.5 million live user connections. As Henk Van Hulle, CEO of Open Banking Limited, put it: "The UK has created something genuinely world-leading." The harder question is why it took 8 years to get there in one country, while globally we're still navigating 30+ incompatible frameworks with no convergence in sight.

Regulation is fragmenting, not converging. The UK succeeded because of consistent governance and trusted standards. The blueprint has been adopted by 60+ jurisdictions, but adoption doesn't mean interoperability. Anyone building cross-border financial infrastructure knows the compliance overhead is still brutal.

AI agents need clean financial data. The interest in structured financial APIs isn't theoretical anymore. We recently added an Agentic Banking section to the tracker, covering banks with MCP (Model Context Protocol) server support. But if we can't agree on data standards after 8 years of Open Banking, how ready are we really for agents acting on financial data autonomously?

Open data has been the right call. The tracker's underlying data is on GitHub. The community catches errors and fills gaps faster than any internal team could. It's not a strategy, it just works.

E-invoicing is underestimated. Mandatory across most of Europe within 5 years. The compliance burden is real, and the overlap with open finance regulation is growing. The Open Finance Map is the first interactive tool that tracks both in one place.

Open Accounting. Open Banking gave consumers control over their bank transaction data. Open Finance extends that to investments, pensions, and insurance. But there's a parallel movement happening that most regulatory maps miss entirely: Open Accounting.

Why this matters now

For Fintechs, the challenge is no longer understanding a single regulation. It's tracking 90+ frameworks at different stages of maturity, across different jurisdictions, with different scopes and timelines. For fintechs expanding internationally, knowing which markets have active open banking APIs versus upcoming mandates versus proposed frameworks is a critical input to market-entry decisions.

The Open Finance Map is live now at openbankingtracker.com/open-finance-map. Free to use, backed by the deepest open banking dataset available anywhere.

Curious what the people who've been in this space longest think: are we actually getting closer to interoperability, or just adding more frameworks?